Ecommerce Financial Reconciliation: 2026 Guide

Your Shopify dashboard says the month was strong. Orders are up, support is busy, and finance is asking a simple question that suddenly isn't simple at all: if sales look good, why doesn't the bank balance line up?

That gap is where most ecommerce teams discover what financial reconciliation really is. It isn't a bookkeeping chore you push to month-end. It's the operating system for trust between your storefront, payment providers, bank account, and accounting records.

In a modern store, a single order can split into multiple financial events. The customer checks out in Shopify. The payment runs through Stripe, PayPal, or another gateway. Fees come out before payout. A refund happens later. A chargeback lands after that. Someone on the support team edits the order post-purchase. By the time money reaches the bank, the original order total is only one piece of the story.

That's why reconciliation keeps moving up the priority list for operators, controllers, and CFOs. The category itself is large and growing. The global reconciliation software market was valued at USD 2.30 billion in 2025 and is projected to rise to USD 2.65 billion in 2026, according to Fortune Business Insights' reconciliation software market analysis. That isn't just a software trend. It reflects a broader shift: businesses are treating reconciliation as infrastructure for control.

In ecommerce, that shift matters even more. High order volume hides small process failures until they become expensive. A messy refund workflow creates accounting noise. Weak tagging on edited orders makes settlements harder to explain. Unclear ownership leaves exceptions sitting open until close week turns into a scramble.

The stores that handle this well usually don't have perfect data. They have a process that catches imperfect data early, routes it to the right owner, and closes the loop fast.

Introduction The Growing Reconciliation Gap in Ecommerce

The reconciliation gap shows up in a familiar way. A merchant sees gross sales in Shopify, expects a similar number to hit cash, then spends hours trying to explain the difference. The answer is almost never one issue. It's a stack of small, operationally normal events that weren't designed to be finance-friendly.

Why ecommerce creates more mismatch than teams expect

Retail used to have fewer handoffs. Ecommerce has many. Shopify records the order. A gateway authorizes and captures payment. A processor batches payouts on its own timeline. Your bank records the deposit. QuickBooks or Xero receives a summarized or synced version of events. Each system is valid within its own scope, but none tells the full story alone.

That's where teams get tripped up. They compare the wrong two records and assume one must be wrong. Often both are right. They're just reporting different stages of the transaction lifecycle.

Practical rule: If your team can't explain the path from order creation to bank deposit in one sentence, your reconciliation process is already under strain.

Why this isn't just an accounting headache

When reconciliation falls behind, the damage spreads into operations. Support teams approve refunds without a standard code. Ops teams edit orders without flagging the financial impact. Finance inherits exceptions with no context and has to reconstruct what happened from notes, tags, and payout reports.

That creates three avoidable problems:

- Slow close: Finance spends time hunting for context instead of reviewing exceptions.

- Weak decisions: Leaders look at sales, cash, and margin views that don't agree.

- Higher control risk: Unreviewed differences can hide timing issues, process errors, or unauthorized activity.

The hard part isn't understanding that numbers should match. The hard part is building a process that still works when your store has edited orders, split captures, partial refunds, shipping adjustments, and delayed payouts.

What Financial Reconciliation Really Means for Your Store

At its simplest, financial reconciliation is the business version of balancing a checkbook. You compare what you think happened against what an outside record says happened. If the balances don't agree, you investigate the variance and correct it.

In a store, though, that simple idea gets bigger fast. You aren't reconciling one ledger against one bank statement. You're reconciling activity across commerce, payments, banking, and accounting. Done properly, it becomes a control system, not just a matching exercise.

The textbook definition is only the starting point

A solid baseline comes from the standard accounting view. Financial reconciliation is a primary control for SOX compliance, comparing internal records such as the general ledger with external sources such as bank statements to ensure balances agree, as described in HighRadius' guide to financial reconciliation. That's why it matters for accurate reporting and audit readiness, not just bookkeeping hygiene.

For ecommerce operators, the practical version is broader. You need confidence that these records connect cleanly:

- Order data from Shopify

- Settlement data from payment providers

- Cash movement in the bank

- Journal entries in QuickBooks, NetSuite, or Xero

If one layer is missing, finance can still post numbers. But the business loses explainability.

What reconciliation tells you that dashboards don't

Dashboards are good at showing activity. Reconciliation is good at proving integrity.

A sales dashboard can tell you an order was placed. It can't always tell you whether the payout arrived in the expected batch, whether processor fees were booked correctly, or whether a support-issued refund was recorded in the right period. Reconciliation answers those questions.

That's also why operators should understand payment rails, not just order flow. If your team needs a clearer grounding in understanding merchant accounts and gateways, it helps explain why the money path and the order path rarely line up neatly.

A healthy reconciliation process doesn't just confirm cash. It confirms that your systems agree on the same commercial reality.

What good looks like in practice

Good reconciliation isn't “everything matches by month-end.” Good reconciliation means:

| Area | What good looks like |

|---|---|

| Ownership | One person prepares, another reviews |

| Evidence | Every exception has support and a resolution path |

| Timing | High-risk accounts are checked before discrepancies age |

| Auditability | Adjustments are documented, not explained in Slack |

| Scope | Refunds, fees, disputes, and edits are included, not treated as side issues |

That last point matters most in ecommerce. Stores don't break reconciliation because sales are high. They break it because the business allows operational exceptions without a financial trail.

Mapping the Modern Ecommerce Reconciliation Workflow

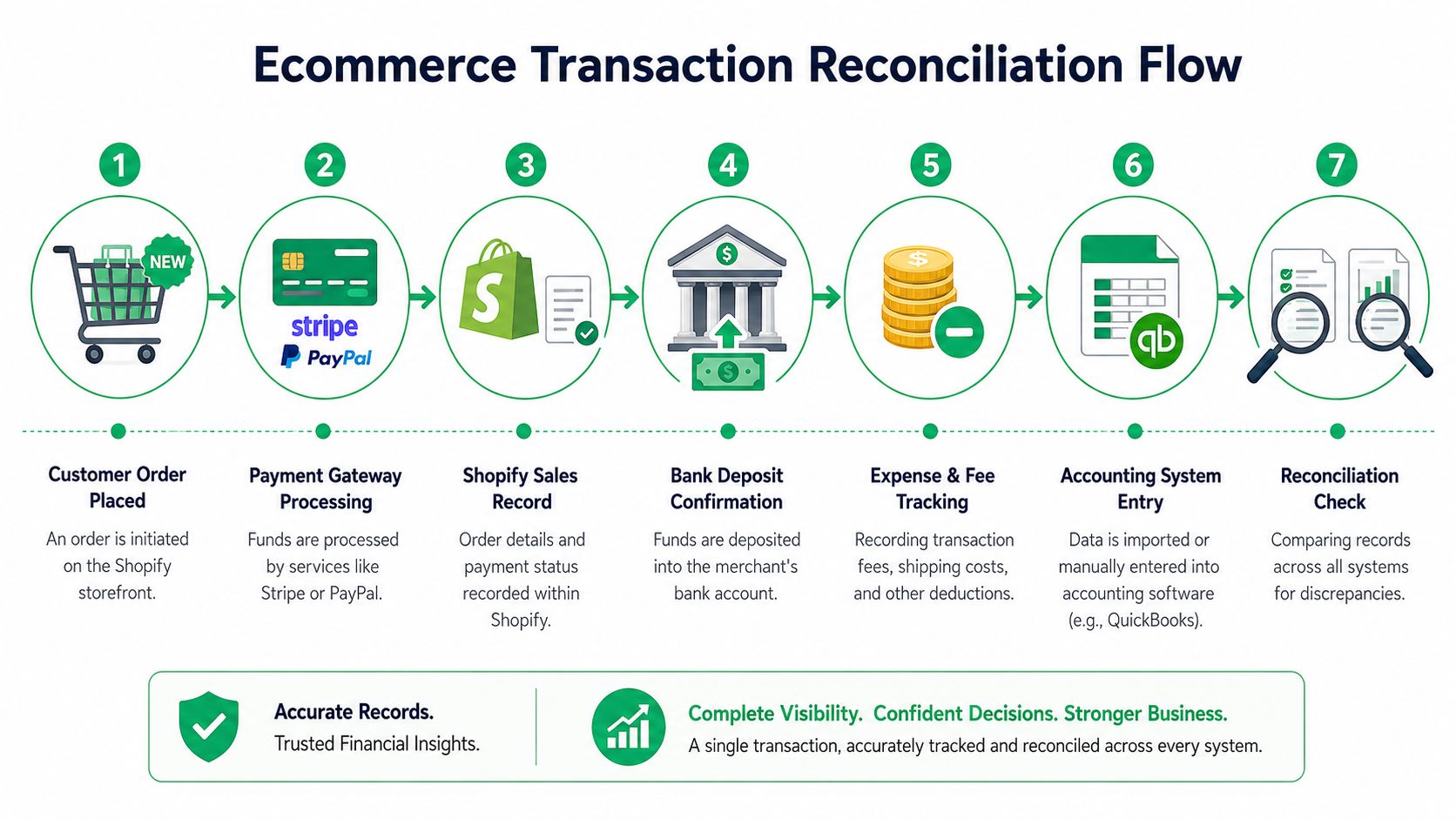

Most reconciliation problems become easier once you trace one transaction all the way through. Start with a single order, not the monthly summary. Follow the money, the metadata, and the handoffs.

The transaction path that finance has to prove

A customer places an order in Shopify. That creates commercial intent. Then a payment provider authorizes or captures payment. After that, the provider settles funds according to its own payout schedule and deducts fees before money reaches the bank. Finally, the accounting system records the event through sync rules, summary journals, or manual review.

That sounds linear, but it rarely stays linear.

Modern reconciliation is a complex data-matching problem across multiple systems that must handle partial refunds, chargebacks, payout delays, and order edits after checkout, as noted in Trintech's explanation of financial reconciliation. In other words, the systems don't just store different views. They record different moments.

Why a 100 dollar order doesn't deposit as 100 dollars

Here's the practical sequence most operators need to map:

- Shopify records the sale with items, tax, shipping, discounts, and order status.

- The payment processor records authorization and capture based on its own rules.

- Processor fees are withheld before payout.

- Refunds or edits may change the order after checkout.

- Disputes may reverse cash later.

- Payouts batch multiple transactions together.

- The bank receives a net deposit, not an order-level mirror.

- The accounting system has to represent all of that cleanly.

That's why teams should define the source of truth by question, not by tool. Shopify may be the source of truth for order intent. Stripe may be the source of truth for settlement detail. The bank is the source of truth for cash movement. The ledger is the source of truth for final financial reporting.

The handoff points where records drift apart

The biggest breaks usually happen at system boundaries.

- Between Shopify and the gateway: an order can change after payment is captured.

- Between gateway and bank: payout timing and fee netting can obscure the link to individual orders.

- Between operations and accounting: manual adjustments get made without standardized notes or tags.

If your team wants a process view of what happens before reconciliation even starts, this breakdown of processing sales orders is useful because upstream order handling decisions shape downstream finance accuracy.

For teams operating internationally, local accounting expectations can also influence how tightly this workflow needs to be documented. A practical reference on financial reconciliation for Australian businesses can help if you're adapting the process across markets.

The fastest way to improve reconciliation is to map exceptions where they originate, not where finance discovers them.

Common Discrepancies and Their Operational Root Causes

Most unreconciled items aren't random. They repeat because the business repeats the same underlying behavior. The visible mismatch is the symptom. The workflow is the cause.

Timing differences are usually process differences

A late-month order may be recorded in one period while the payout lands in the next. A refund approved today may settle later. A chargeback may appear long after the original sale. None of those mean the systems are broken.

What matters is whether your team classifies them correctly and keeps them visible until they clear.

Unresolved timing differences become fake mystery items when nobody owns the carry-forward process.

Teams get into trouble when they treat timing differences as one-off anomalies. In reality, they're recurring categories that need rules. If your close depends on someone remembering which payout spilled into the next period, the process is too fragile.

Refunds expose weak operating discipline fast

Refunds create reconciliation noise because they often bypass standard paths. Support may issue them manually. Ops may approve an order change without a structured reason code. Finance then sees reduced settlement cash and has to figure out whether the reduction came from a valid refund, a fee, a dispute, or a posting error.

For Shopify-heavy teams, the operational side of that matters as much as the accounting side. A documented refund workflow in Shopify helps because finance needs clean event history, not just a final net number.

Governance failures create the hardest discrepancies

The most stubborn reconciliation issues usually involve role confusion. University guidance on reconciliation and review stresses that the reconciler should not be the same person making purchases, reinforcing that the core challenge is governance, role separation, and escalation design, not just matching numbers, as outlined by the University of Kentucky's reconciliation and review guidance.

That principle applies directly to ecommerce operations. If the same person can edit orders, issue refunds, and mark exceptions resolved, your controls are weak even if the books eventually tie out.

A few root causes show up repeatedly:

- Unclear ownership: nobody knows whether support, finance, or ops should investigate a mismatch.

- Manual order edits: staff change item values, shipping, or discounts without a standard audit trail.

- Loose approval paths: exceptions are cleared informally in chat instead of through documented review.

- Backlog tolerance: old items stay open because there's no aging discipline.

- Reviewer bias: the preparer explains their own exception and the reviewer rubber-stamps it.

Hidden fees and net settlements distort assumptions

Finance teams often compare gross sales to net deposits and then burn time proving what was already predictable. Processor fees, cross-border costs, dispute deductions, and batched settlements all compress the detail before cash reaches the bank.

The answer isn't more spreadsheet work. The answer is designing the process so the netting logic is expected, documented, and reviewable before month-end.

Automation and Tooling Strategies for Scalable Ops

Spreadsheets can work for a while. Then volume rises, exception counts grow, and the same flexibility that made spreadsheets useful starts breaking control. Tabs multiply, versions drift, and the team spends more time proving which file is current than resolving the actual discrepancies.

The right tooling depends on complexity, not ambition. Some stores need better exports and cleaner operating rules. Others need dedicated reconciliation software.

The four maturity stages most ecommerce teams move through

| Stage | Typical setup | Works well when | Starts failing when |

|---|---|---|---|

| Manual | Shopify exports, gateway reports, spreadsheet tie-outs | Volume is low and exceptions are limited | One person becomes the bottleneck |

| Connected | Basic syncs into QuickBooks or Xero | Transactions follow predictable patterns | Refunds, edits, and disputes increase |

| Operationally structured | Standard tags, reason codes, owner queues, exception logs | Teams need repeatability across departments | Manual review still dominates close |

| Purpose-built automation | Reconciliation platform with matching rules and audit workflow | Multi-system complexity is high | Bad source data still enters upstream |

What to automate first

Don't start by automating everything. Start with the highest-frequency, lowest-judgment work.

- System exports and imports: remove copy-paste steps between Shopify, gateways, and accounting.

- Exception tagging: flag edited orders, manual refunds, and disputed transactions consistently.

- Owner assignment: route mismatches to support, ops, or finance based on type.

- Documentation capture: keep evidence attached to the exception, not buried in inboxes.

- Review workflow: separate preparation from approval wherever possible.

A lot of teams think they need better finance tooling when they need better upstream order discipline. If your order workflows are loose, even the best reconciliation software will inherit messy data. This is why an operationally sound Shopify order management system matters before finance tries to automate the back end.

How to evaluate tools without overbuying

Tool selection should follow three questions.

First, where is the actual break? If the issue is fee visibility, you may need better payment reporting. If the issue is exception ownership, workflow software may matter more than matching logic. If the issue is auditability, approval controls become the priority.

Second, what is your source of truth per event type? A tool that imports everything but preserves no ownership model won't solve much.

Third, can the team support the rule set? Every automated match rule needs maintenance. If nobody can explain why the system matched or excluded a transaction, you've traded one opaque process for another.

Operator's test: If a new controller joined tomorrow, could they tell where to look for fees, refunds, edits, and payout timing without asking three different teams?

What doesn't scale

A few habits fail almost every time:

- Monthly-only investigation: by then, the people who made the decisions may not remember them.

- One giant reconciliation file: it becomes both system of record and black box.

- No exception taxonomy: everything gets labeled “difference,” which tells nobody what to do next.

- Sync first, process later: integrations don't fix undefined workflows.

Practical Reconciliation Tips for Shopify Merchants

Shopify merchants can reduce a lot of reconciliation pain before finance ever touches a statement. The best fixes usually happen in support, fulfillment, and post-purchase workflow design.

Use operational signals that finance can actually read

If your team edits orders after checkout, don't leave that activity buried in timelines and agent notes. Create a tagging standard that finance can filter.

Useful examples include:

- Edited order

- Manual refund

- Address correction

- Reship

- Customer appeasement credit

- Chargeback received

The exact tags matter less than consistency. Finance needs to know which transactions deserve exception review without reading every order note one by one.

Treat address quality as a finance issue

Bad addresses look like a fulfillment problem until the downstream costs hit. Reships, canceled labels, manual shipping adjustments, and customer service credits all create financial noise that later has to be explained. Clean address capture reduces preventable exceptions before they become ledger cleanup.

That's one reason post-purchase controls matter so much in Shopify. If customers can correct details inside a governed workflow instead of through ad hoc support messages, the audit trail gets cleaner.

Standardize refund reasons and order edit approval

Most stores let refunds happen faster than they let documentation happen. That's backwards. Speed matters, but a fast refund with weak metadata creates slow reconciliation later.

A better pattern looks like this:

- Require a reason code for every refund or credit.

- Separate approval rules for discretionary refunds versus policy-based ones.

- Flag partial refunds for review because they create more interpretation risk.

- Link the action to the order event, not just the payment event.

This walkthrough is worth sharing with the team during process training:

Keep edited orders from becoming invisible

Order edits are one of the easiest ways to create a mismatch between commerce records and settlement data. If support changes items, shipping, or totals after checkout, the store needs a standard path for documenting what changed and whether the payment record changed too.

A few habits help immediately:

- Log the business reason: not just “customer request,” but what changed and why.

- Record who approved it: especially when the change affects value.

- Review edited orders daily: don't let them pile into month-end.

- Escalate mismatched payment outcomes: if the order changed but settlement didn't, finance should know quickly.

Shopify stores don't need perfect simplicity. They need visible exceptions.

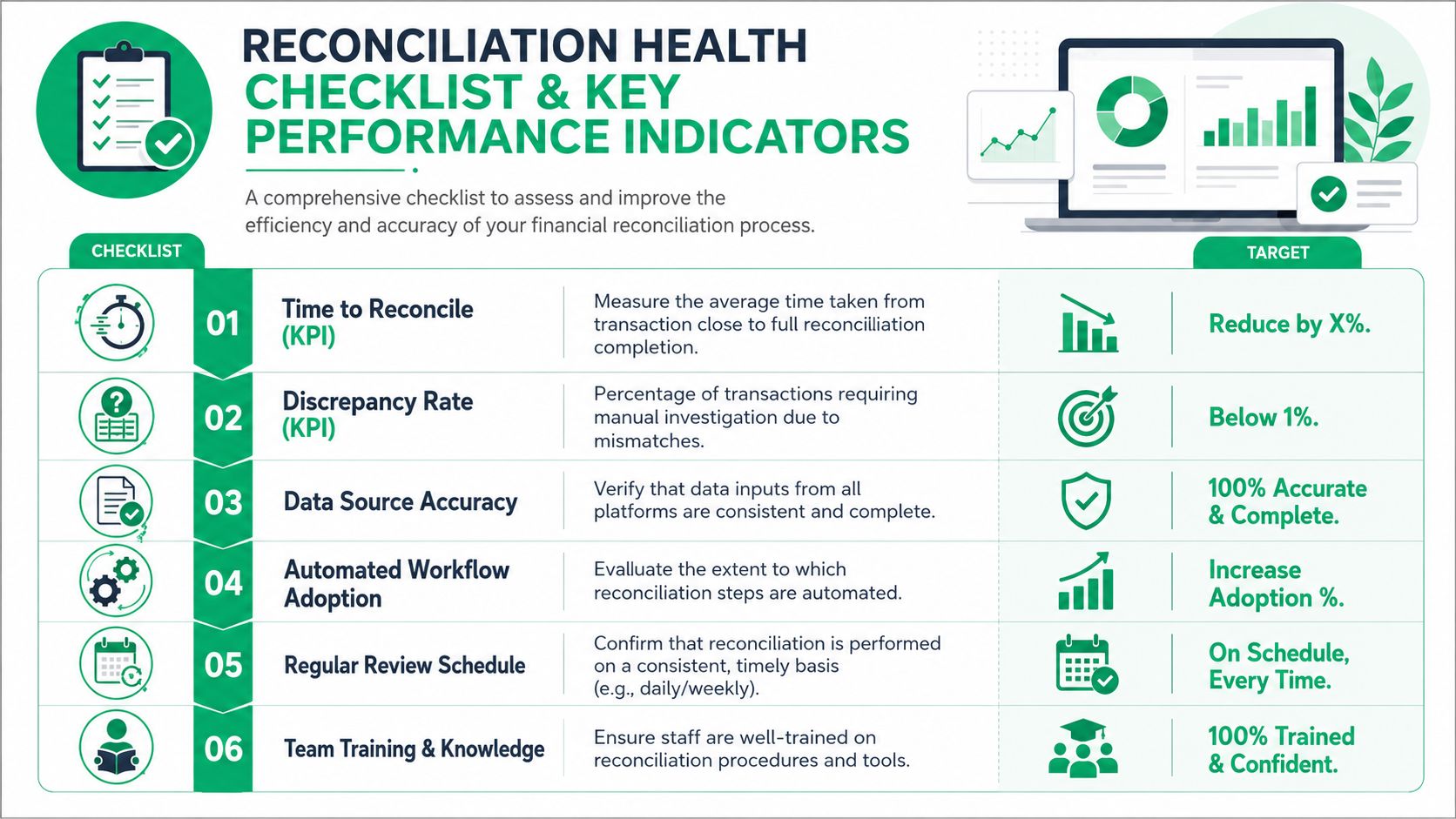

KPIs and Your Reconciliation Health Checklist

You can't improve reconciliation by feel. You need a small set of measures that show whether the process is tight, late, or drifting.

The best KPIs aren't vanity metrics. They help a controller, finance manager, or ops lead see where friction is accumulating.

The KPIs that actually tell you something

A useful scorecard usually includes:

- Time to reconcile: how long it takes from transaction activity to reviewed completion

- Open unreconciled items: the queue that still needs explanation

- Average age of discrepancies: whether your team is resolving issues promptly or carrying them forward too long

- Manual exception volume: how much work still depends on human investigation

- Reviewer turnaround: whether approvals are flowing or getting stuck

These don't need to be fancy. They need to be reviewed consistently and tied to owners.

Frequency should follow risk, not habit

A practical benchmark is to set reconciliation cadence by account risk and transaction velocity. High-volume cash and payment accounts should be reconciled daily, while lower-volatility accounts can be reconciled monthly, as outlined in Numeric's guide to account reconciliation. That approach catches discrepancies earlier and protects control integrity.

For ecommerce teams, that usually means daily attention on cash, processor settlements, and refund-heavy channels. Slower-moving balance sheet accounts can follow a lighter schedule if they aren't exception-prone.

Review frequency should be based on how quickly an account can go wrong, not how long the team has historically waited.

A practical checklist for operators and finance leads

Use this as a live health check, not a one-time project list.

Process checks

- Owners are defined: each account and exception type has a named preparer and reviewer.

- Exception categories exist: timing, refund, fee, dispute, edit, and sync issues aren't lumped together.

- Aging is visible: old items can't hide inside current-period work.

- Close rules are clear: the team knows what can be carried forward and what must be resolved now.

System checks

- Source systems are named: Shopify, gateway, bank, and ledger roles are explicit.

- Reports are reproducible: nobody depends on one analyst's private spreadsheet logic.

- Supporting evidence is attached: documents live with the reconciliation record.

- Automation is selective and explainable: the team trusts the match rules because they understand them.

Governance checks

- Preparation and review are separated: nobody self-approves sensitive reconciliations.

- Escalation paths exist: edited orders, partial refunds, and unexplained net deposits have a route.

- Old discrepancies are revisited: carry-forward items don't become permanent clutter.

- Operations and finance meet regularly: exception trends are fixed upstream, not just cleared downstream.

If a team can answer yes to most of those without hesitation, the reconciliation process is probably healthy. If every answer depends on one experienced employee, it isn't.

If post-purchase order changes are creating reconciliation noise in your Shopify store, SelfServe helps reduce that mess at the source. It gives customers controlled ways to update order details, supports address validation, and adds structure to post-purchase workflows so ops teams handle fewer ad hoc exceptions and finance gets cleaner downstream records.